Firehose #188: 🛢 Payment tech is motor oil. 🛢

How payment tech lubricates marketplaces. Plus: Squarespace goes public, the media cycle, Apple's dominance with teens, and more!

One Big Thought

Inspiration for this newsletter comes from all over the place.

I save articles all week long to read over the weekend, and those form most of the topic base for Firehose. In addition, I sometimes draw inspiration from a tweet, a blog post, or a conversation I’ve had with a founder. Occasionally, one of my partners says something so insightful in a meeting that I just have to write about it.

This week’s inspiration comes from a stranger source — a piece of marketing material from a wealth management firm. Bessemer Trust sends out a Quarterly Investment Perspective, and this past one was on the topic of “The Future of Money.” It’s quite good and can be accessed online here.

A particular section stood out to me, which I’ll quote verbatim:

E-COMMERCE AS THE PAYMENTS INCUBATOR

A virtuous cycle exists when an online marketplace is met by robust digital payments infrastructure. In many cases, the former precedes the latter. In those instances, the marketplace platform has served as an incubator for a payments solution that ultimately extends far beyond the confines of its initial host. This playbook has been adopted globally, much to the benefit of shareholders given its track record of significant value creation, often stemming from expansive growth of these once-incubated payments platforms.

The piece then goes on to discuss the canonical example of the intersection of payments and marketplaces — EBAY/PYPL*:

In 2002, eBay was processing ~$13 billion in merchandise annually. However, 60% was paid for by check or money order, and the sellers usually waited for the checks to clear before shipping their items, resulting in a transaction process that could take as long as two weeks. PayPal’s technology, by contrast, allowed consumers to make and accept payments over the internet without using a credit card, with the bulk of its business coming from eBay auctions. eBay acquired PayPal for $1.5 billion that year, removing friction from the eBay buying process and supporting the virtuous cycle of marketplace network effects. While eBay continued to scale its auction platform, PayPal expanded to the other merchants and has participated directly in the large and growing addressable market of online commerce.

If marketplaces are engines, then payment tech is motor oil. Removing friction from an economic engine lets it work harder and faster. PYPL accelerated EBAY’s network effects by lubricating transactions, and that lower friction translated into more profits and growth.

The article goes on to discuss other global examples:

BABA* launched Alipay’s escrow service in 2004 to solve trust problems in its B2C marketplace Taobao, which launched a year prior. Alipay eventually enabled users to do more with their account balances, supporting lending, wealth management, insurance products and more today.

MELI* launched in 1999 to a largely unbanked population in LATAM. Over the next decade, its MercadoPago product rolled out to absorb 1/3rd of transaction volume on the platform. Today it covers nearly all transactions on platform and also supports a significant number of off platform transactions.

SE* launched in 2015 in Singapore, and its Shopee platform has grown into an e-commerce leader in Southeast Asia. 70% of the region’s population is unbanked or underbanked, so SE launched SeaMoney, a mobile wallet that has grown to 30% of gross orders last October.

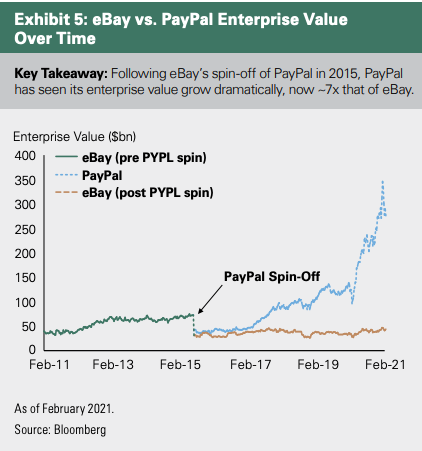

Money has gravity. Once users start to accumulate a balance of local currency, the friction is lowest to spend it on the platform itself, or on services directly linked to the platform. That’s why BABA, MELI, and SE have all shown success bringing tightly integrated, non-marketplace use cases to their digital wallet users. While payment tech starts as the lubricator of the marketplace, eventually it forms the foundation of new use cases. That means consumer payments, when incubated inside a marketplace, often become bigger than the marketplace itself. As noted in the Bessemer Trust report, PYPL is now 7x more valuable than EBAY, 6 years post-spinout:

These observations also have implications for the emerging wave of B2B and wholesale marketplaces I discussed last week.

SMB payment tech is quite far behind where consumer payments sit today. We should expect that much of the innovation in lending, insurance, factoring, and other financial services for SMBs will come from marketplaces, not neobanks. In fact, due to the difficulties some B2B marketplaces have extracting sizable take rates (again, read my post from last week!), you might expect digital payments to be the dominant monetization model in the category. Fintech infrastructure providers like Finix* and Synctera* (both Lightspeed portfolio companies) should see strong uptake in the B2B marketplace category as these businesses arm themselves with payments features.

If you see great examples of B2B marketplaces deploying payments tech, please send me a note. I’d love to feature them in the coming weeks.

Tweet of the Week

Links I Enjoy

#commerce

![[MISSING IMAGE: tm218193d1-pg_01square4c.jpg]](https://substackcdn.com/image/fetch/$s_!raNe!,w_1456,c_limit,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2Fed28c442-18e1-4eaa-8147-0ba6d47381eb_1262x1620.jpeg "[MISSING IMAGE: tm218193d1-pg_01square4c.jpg]")

Hip to be Squarespace.→

Squarespace filed its S-1 after nearly two decades as a private company. The prospectus identifies over 800M small businesses globally in its target market, and notes that half a million of these are started each month just in the US. 46% of small businesses are not online today.

Squarespace has 3.6M unique subscribers at a $187 ARPU. When your ARPU is that low, you need to establish a hyper efficient go-to-market strategy. With over $152M of free cash flow and a “Rule of 40” number of 52%, Squarespace has both growth and profitability dialed in.

#media

The media clock. →

Someone on Twitter shared this old Wired article by Aaron Zamost of Square*. It’s just as relevant in today’s media environment. Aaron’s metaphor is a clock. In my conversations on this topic, I’ve often thought of media as a pendulum that swings from friend to foe. Because media needs to create conflict to drive engagement, it often builds up a company in order to knock it down later. Then it loves to tell the redemption story.

Unfortunately, it’s quite hard to opt-out of this model. So instead startups need to embrace the cycles and understand where they are in it. Planning for the inevitable crisis also helps navigate through the fog of war when it eventually happens.

#tech

Apple’s dominance with teens. →

Airpods launched in 2016 to confusion and jeers. I think I might have called them “ear cigarettes” at some point. But when I tried them, I instantly fell in love. Airpods are the best product Apple* has created since the iPhone.

The teens agree. A whopping 70% (!) own a pair (up from 52% a year ago), slightly less than the 88% who own an iPhone. Only 34% of teens own a smart watch, but 84% of those who do own an Apple Watch. Apple’s utter dominance with teens, and the seamless interoperability between its devices, means that it’s quite unlikely they shift to Android in later years.

#science

Muon along. →

We don’t encounter new physics very often, and when we do, the results are often attributed to experimental or human error. Scientists recently observed muons in a particle collider oscillating at a rate not explained by the Standard Model of physics. That would suggest the presence of a particle or force not yet predicted by the Standard Model. The measurements have only a 1 in 40,000 chance of being a fluke, or something like 4 standard deviations from the mean.

#culture

Edible art. →

I’ve been baking a lot during quarantine. It appeals to my inner chemist and somehow breaks up the monotony of sitting in my house all week. My kids also love getting their hands into the ingredients and getting to consume the results of their labor!

As the YouTube algo has adjusted to my new passion, I come across videos like these which are mesmerizing. I would never have the patience to make something this intricate, but admire those who do.

Enjoyed this newsletter?

Getting Drinking from the Firehose in your inbox via Substack is easy. Click below to subscribe:

Have some thoughts? Leave me a comment:

Or share this post on social media to get the word out:

Disclaimer: * indicates a Lightspeed portfolio company, or other company in which I have economic interest. I also have economic interest in AAPL, ABNB, ADBE, ADSK, AMT, AMZN, BABA, BRK, BLK, CCI, COUP, CRM, CRWD, GOOG/GOOGL, FB, HD, LMT, MA, MCD, MELI, MSFT, NFLX, NSRGY, NEE, NET, NFLX, NOW, NVDA, PINS, PYPL, SE, SHOP, SNAP, SPOT, SQ, TMO, TWLO, VEEV, and V.